Many brands evaluate contract manufacturers on formulation capability and cost. Geography comes up later, usually when it’s already showing up in their numbers.

A brand does everything right. They find a manufacturer with real formulation capability, someone who can handle the chemistry, hit the spec, and scale reliably. The product launches. Retail accounts follow. And then a different kind of problem surfaces: safety stock that keeps creeping up, working capital tied to product in transit, delivery windows that don’t have enough buffer when demand moves unexpectedly. The formula is right. The manufacturing is solid. The geography is quietly costing them.

Where your manufacturing partner sits shapes your inventory levels, your working capital requirements, your service levels, and your ability to respond when something changes. It shows up in your numbers whether you planned for it or not. And in 2026, with brands actively restructuring supply chains for resilience and domestic manufacturing gaining real strategic ground, the location decision has moved from operational footnote to boardroom conversation.

The 2026 Supply Chain Reset

After two years of tariff uncertainty, supply chains are entering a phase that looks less like chaos and more like manageable complexity. Tariff rules are better understood and largely embedded in most companies’ costs and strategies. Instead of scrambling to respond, supply chain leaders are now managing within largely known constraints.

What that shift is producing: deliberate structural decisions about where to manufacture and how to build resilience that weren’t possible when policy was changing month to month. As industries see significant reshoring activity, the total cost of ownership calculation, one that factors in tariff exposure, inventory carrying costs, transit time, and risk, is landing differently than it did five years ago.

Companies have announced more than $1.7 trillion in new manufacturing investments, with significant activity in Tennessee. The investments made during the height of tariff uncertainty have set companies up for a structural advantage going forward. Resilience has moved from cost center to core strategy. A domestic manufacturing partner with genuine formulation depth, positioned in a logistics-dense market, is one of the most direct expressions of that strategy.

Why Formulation Capability Has to Come Before Logistics Speed

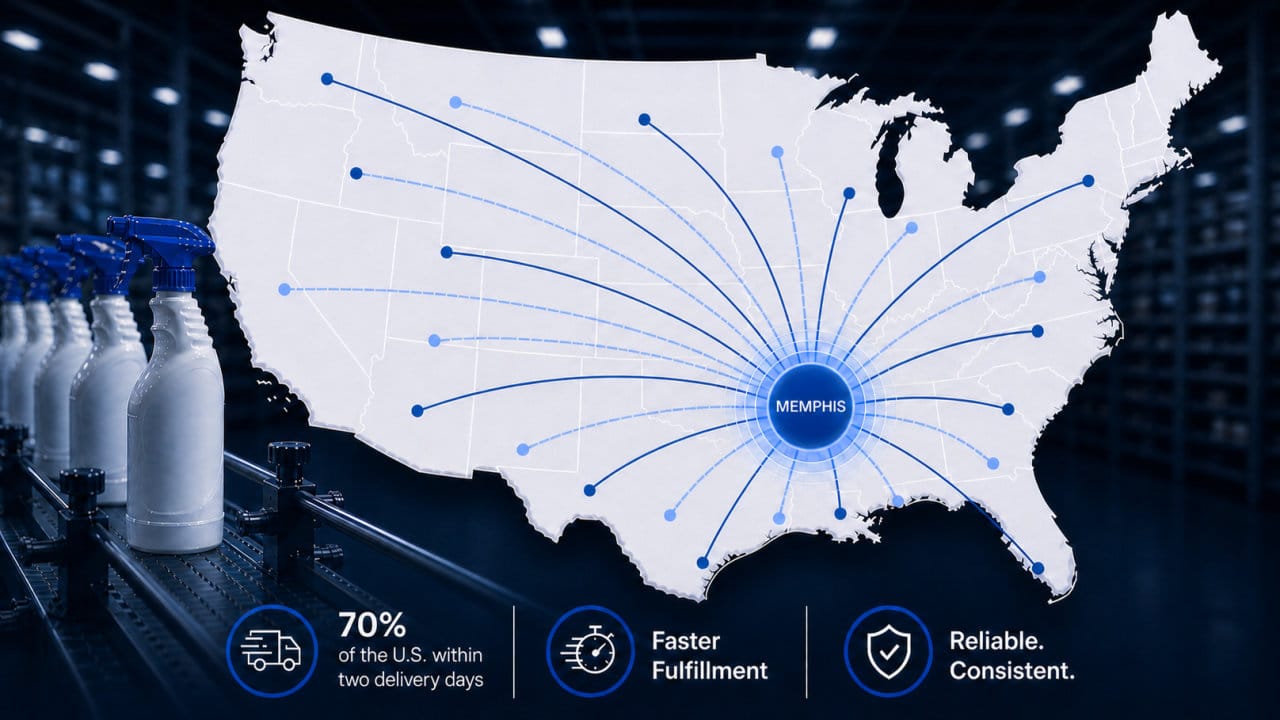

Getting product to shelf fast starts with getting the product right. BPI’s integrated facility — formulation, blend-and-fill, and distribution under one roof — is built for both, and our Memphis location puts 70% of the U.S. within two delivery days.

That combination matters because speed without manufacturing discipline isn’t an advantage. BPI operates with two PhD formulation scientists on staff and 36 shelf-ready formulations, solving complex chemistry problems that most blend-and-fill operations can’t or won’t touch. For brands across home care, automotive appearance, industrial, and consumer product categories, where formulation complexity, retail compliance, and speed to shelf all intersect, that’s not a logistics story. It’s an integrated capability story, from concept to shelf, with the reach to back it up.

How Transit Time Affects Inventory Costs and Working Capital

Trucks leaving Memphis can reach 40% of the U.S. population overnight and 75% within two days. Home to the world headquarters and world hub of FedEx and major UPS, DHL, and U.S. Postal operations, Memphis provides access to the most cost-effective distribution infrastructure in the nation. Recent investments represent active, ongoing commitments to efficiency that continue to strengthen Memphis’s position as a central distribution node. This isn’t legacy infrastructure coasting on reputation. It’s being actively built out.

But the reason this matters for your business isn’t the infrastructure itself. It’s what transit time actually costs you.

Every extra day a shipment spends in motion is a day your inventory isn’t at the retailer. To compensate, you carry more safety stock. More safety stock means more cash tied up in product sitting in a warehouse. More cash tied up means less flexibility – to respond to a demand surge, to fund a new SKU launch, to take a retail opportunity when it arrives.

Run it in reverse: a manufacturing partner in a central, high-velocity logistics hub means shorter transit to most of your retail DCs. Shorter transit means leaner inventory. Leaner inventory means better cash flow and more room to grow. This is a financial argument, not a logistics one, and it rarely gets asked during a manufacturing partner evaluation with the rigor it deserves.

Memphis sits within one to two days of the major retail distribution hubs that matter most to consumer brands: Walmart’s Bentonville network, Target’s Minneapolis DCs, and Amazon fulfillment centers across the Southeast and Midwest. For brands shipping nationally, that’s not a minor convenience. It has a direct impact on working capital.

Here’s a simple illustration. A brand doing $1.5M in annual sales with a 45-day average order-to-delivery cycle has roughly $185,000 tied up in transit and pipeline inventory at any given time. Shave five days off that cycle, a realistic outcome when your manufacturer is two days closer to your retail DCs than the industry average, and that figure drops to approximately $164,000. That’s $21,000 in working capital freed up on a single product line, without changing your sales volume, your pricing, or your retail relationships.

For a brand managing five to ten SKUs across multiple retail accounts, the effect compounds. And it shows up not just in cash flow, but in your ability to respond to demand signals, reorder faster, and avoid the out-of-stock penalties that carry their own compliance costs.

Geography, OTIF Compliance, and Retail Delivery Windows

Retail compliance pressure — automated OTIF enforcement, tighter delivery windows, system-triggered chargebacks — deserves its own conversation, and it’s one worth having separately. What geography adds to that picture is simple: response time. When something changes, how quickly can your manufacturing partner react?

When your manufacturer is two or three extra transit days from your retail DCs, you’re operating with a structural disadvantage on every order. You need more lead time, more safety stock, and more margin for error, and you still may miss the window when something unexpected happens. Proximity compresses that risk at every level: the ability to reorder quickly when a SKU runs hot, to respond to a fill-rate request without a two-week lag, to turn around a packaging update without waiting through a long production and transit cycle.

Location isn’t about convenience, it’s about reach, responsiveness, and risk mitigation. Geography turns into velocity, infrastructure into resilience, and complexity into consistency.

What to Ask Your Contract Manufacturing Partner About Location

Many brands, when evaluating a manufacturing partner, ask about capabilities, pricing, minimums, and lead times. Those are the right questions. Formulation capability and quality track record have to come first, they’re non-negotiable.

But the geography question — where does this partner sit relative to where my product needs to go, and what does that mean for my inventory, my service levels, and my cash flow — is rarely asked with the same rigor. It should be. Because the answer shows up in your numbers every month, whether you planned for it or not.

BPI combines formulation expertise and blend-and-fill capability under one roof, with an average order-to-delivery of 30 days, and a location that puts 70% of the U.S. within two delivery days. 100% of our clients have been with us for more than two years, building on a foundation that includes not just what we can make, but how reliably and quickly we can get it where it needs to go.

If you’re rethinking your manufacturing footprint in light of what the last two years have done to supply chain economics, we’d like to be part of that conversation.

BPI Solutions helps brands bring products from concept to shelf with formulation support, blend-and-fill operations, packaging, and distribution. Learn more at www.bpipackaging.net.

Sources:

Transimpact — New Tariffs, New Timeline: Preparing Your Supply Chain for the 150-Day Countdown https://transimpact.com/blog/new-tariffs-new-timeline-preparing-your-supply-chain-for-the-150-day-countdown

Supply Chain Management Review — Six Months In: Are Tariffs Really Rebuilding American Manufacturing? https://www.scmr.com/article/tariffs-us-manufacturing-reshoring-impact-2025

Gray Group International — Supply Chain Resilience in 2026: How Smart Businesses Are Navigating the Tariff Storm https://www.graygroupintl.com/blog/supply-chain-resilience-2026-tariff-strategy/

Averitt — Memphis’ Role as a Key International and Domestic Logistics Hub https://www.averitt.com/blog/memphis-logistics-hub

Memphis Moves — Supply Chain + Logistics Industry https://memphismoves.com/industries/supply-chain-logistics/

REBusiness Online — Memphis: A World-Class Logistics Hub Positioned for Future Growth https://rebusinessonline.com/memphis-a-world-class-logistics-hub-positioned-for-future-growth/

Supply Chain Dive — In Logistics, All Roads Lead to Memphis https://www.supplychaindive.com/news/logistics-hub-memphis-fedex/563674/

LifeScience Logistics — Location, Location, Location: The Importance of a Specialized, Strategic Hub for Healthcare Distribution https://www.lslog.com/importance-of-a-specialized-strategic-hub-for-healthcare-distribution/